Why Global Mobility Demands Smarter Financial Strategies

As an expat, the world truly is your oyster – offering unparalleled opportunities for personal and professional growth. Yet, with global mobility comes a unique set of financial complexities, particularly when you seek to grow and protect your wealth across international borders.

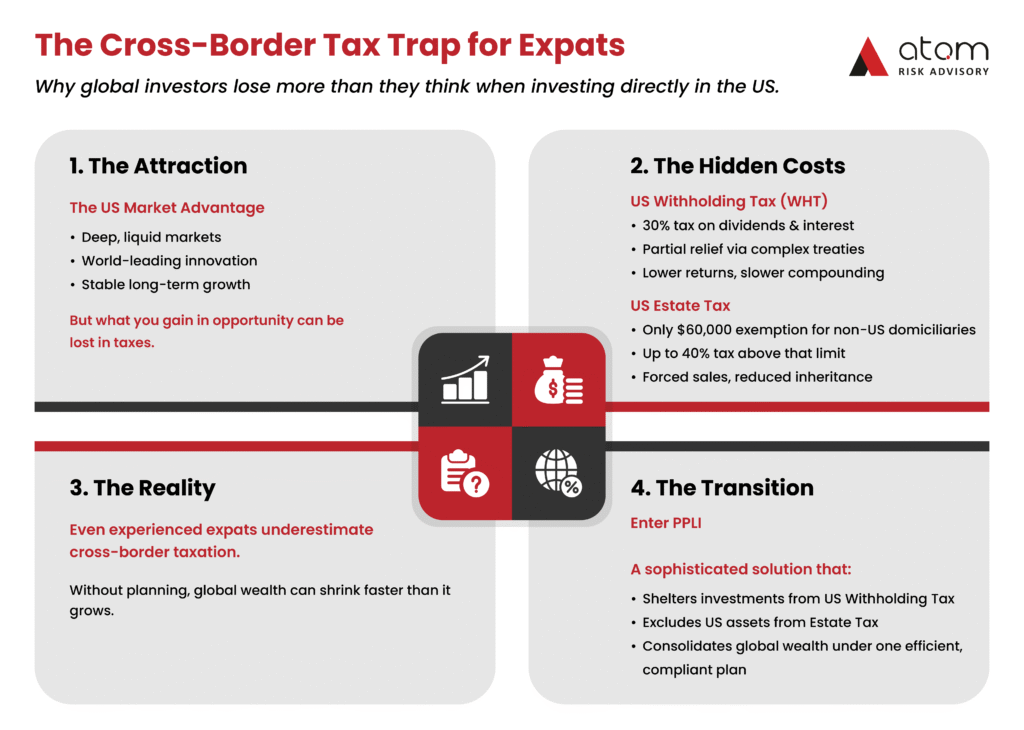

You’re likely drawn to the stability and growth potential of the US market, whether through its robust equities, secure bonds, or attractive property investments.

But here’s the often-overlooked challenge: without strategic planning, the very wealth you work hard to build can be eroded by unexpected US tax liabilities, particularly Withholding Tax and Estate (Inheritance) Tax. These hidden costs can significantly impact your returns and compromise your legacy.

What if there was a sophisticated yet elegantly simple solution to navigate these cross-border complexities – one that not only protects but optimizes your wealth for generations to come?

Welcome to Private Placement Life Insurance (PPLI) – the ultimate wealth shield for global expats.

Unlocking US Market Growth: The Withholding Tax Dilemma for Expats

The allure of the US financial markets is undeniable. Their size, liquidity, and global innovation make them a magnet for international investors. For Indian and UK expats, investing in US equities and bonds offers diversification, potential for higher returns, and exposure to world-leading companies.

However, many expats encounter a major hurdle – US Withholding Tax (WHT).

When you, as a non-US resident or non-US domiciliary, invest directly in US-sourced assets, the Internal Revenue Service (IRS) typically imposes a 30% withholding tax on income such as dividends and interest. While some tax treaties (such as between the US and UK or India) may reduce this rate, the administrative burden of claiming treaty benefits can be cumbersome, and residual liabilities often remain. Additionally, certain capital gains may still attract US taxes, depending on your residency status and the type of asset.

This means a significant portion of your investment income may be withheld before reaching you – reducing your compounding power and overall returns. It’s a silent drain on wealth accumulation that makes direct US investments less efficient than they appear.

Expat Property & Inheritance Tax: Protecting Your Legacy Across Borders

Beyond financial markets, many expats are drawn to US property ownership – whether for rental income, vacation use, or long-term investment. Yet this too comes with hidden complexity: US Estate (Inheritance) Tax.

The US estate tax regime is particularly harsh for non-US citizens who are not domiciled in the US.

While US citizens enjoy a generous exemption exceeding USD 13 million, non-US domiciled individuals are entitled to a mere USD 60,000 exemption on their US situs assets. Anything above that threshold can be taxed at rates up to 40%.

Imagine owning prime US real estate worth millions – only for your beneficiaries to face a crippling tax bill upon your passing. This often leads to forced asset sales, complex estate administration, and unintended erosion of legacy.

For Indian and UK expats, whose home countries may also levy inheritance taxes, the double exposure can be severe. Effective cross-border estate planning is therefore essential to preserve family wealth and ensure smooth succession.

This is where Private Placement Life Insurance (PPLI) stands out as a sophisticated yet remarkably effective solution for high-net-worth (HNW) expats.

PPLI Explained: Your Global Solution to Tax & Estate Complexities

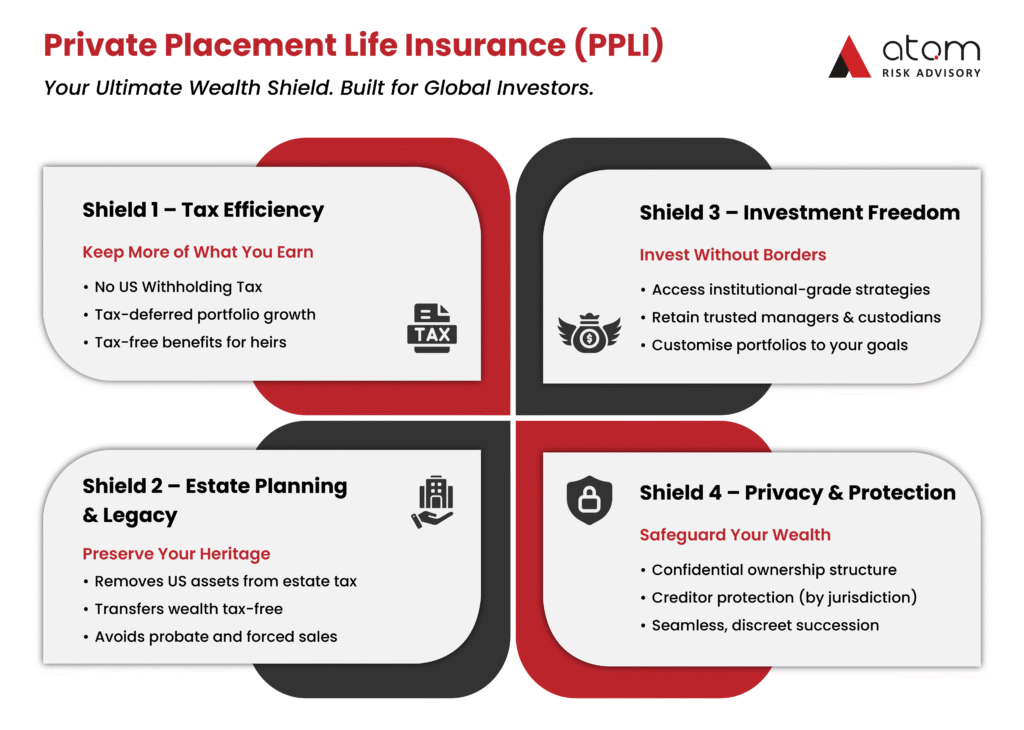

PPLI is not traditional life insurance – it’s an institutionally priced, customizable variable universal life contract designed for affluent investors seeking tax optimization, asset protection, and seamless estate planning across multiple jurisdictions.

- Mitigating US Withholding Tax on Investments

- Tax Deferral & Elimination:

When you invest through a PPLI policy, your assets (equities, bonds, alternatives) are held within the insurance wrapper. Because the policyholder of these assets is typically a non-US insurance carrier, income from US investments (dividends, interest, capital gains) is generally not subject to US Withholding Tax for non-US persons.

This allows your portfolio to grow tax-deferred, compounding faster over time. Upon death, the policy’s value is typically paid out tax-free, making it a powerful wealth-accumulation tool. - Simplified Tax Reporting:

Instead of dealing with complex WHT forms or treaty claims for each holding, PPLI consolidates your US-sourced income into a single, tax-efficient structure, dramatically easing compliance.

- Bypassing US Estate (Inheritance) Tax on Property & Other Assets

- Excluding Assets from the Taxable Estate:

For non-US domiciled expats, PPLI can remove US situs assets (including property, stocks, and bonds) from your taxable estate. This is achieved by holding the assets through an entity owned by a PPLI policy or by purchasing US property via a foreign trust funded by the policy. These assets are therefore not considered part of your US estate. - Tax-Free Transfer to Heirs:

On death, the PPLI death benefit is typically paid to beneficiaries free of US income and estate tax. This bypasses the harsh 40% tax rate and the $60,000 exemption cap, preserving your legacy, avoiding forced sales, and ensuring efficient wealth transfer.

- Additional Advantages of PPLI

- Investment Flexibility:

PPLI gives access to institutional-grade investment strategies and allows you to work with your preferred asset managers, while keeping assets within your existing custodian bank. - Asset Protection:

Depending on the issuing jurisdiction, assets inside a PPLI policy may enjoy creditor protection, shielding them from future claims.

- Privacy, Confidentiality & Estate Planning Efficiency

- Enhanced Privacy:

PPLI ensures a higher level of confidentiality, as assets are held within the insurance wrapper rather than in your personal name. - Streamlined Estate Planning:

It simplifies the transfer of wealth to heirs, avoiding lengthy, public, and costly probate procedures – especially valuable for expats with assets across multiple countries. - Liquidity Options:

While designed for legacy and long-term growth, PPLI policies can offer liquidity through loans or withdrawals, subject to careful tax and benefit considerations.

Secure Your Future, Beyond Borders

For globally mobile professionals investing in the US or owning US assets, Withholding Tax and Estate Tax can pose real threats to wealth preservation.

With Private Placement Life Insurance, these challenges can be turned into strategic opportunities.

PPLI offers a robust, tax-efficient, and confidential structure that helps you grow, protect, and transfer wealth seamlessly, thereby empowering you to secure your family’s future no matter where you call home. It’s more than insurance; it’s a cornerstone of modern global wealth management.

Take the Next Step with Atom Risk Advisory

At Atom Risk Advisory, we specialize in cross-border life insurance solutions designed for globally mobile clients, business owners, and family offices. Our team collaborates with leading international carriers and fiduciary partners to craft structures like PPLI and VUL (Variable Universal Life) that optimize tax efficiency, asset protection, and legacy continuity.

Whether you are an Indian expat in the UAE, a UK resident investing in the US, or a global family seeking intergenerational protection, our experts can help you design a bespoke plan tailored to your goals.

Talk to our advisory team today to explore how PPLI can transform your global wealth and estate strategy.