Critical illness is no longer just a medical event. It is a financial one. As healthcare costs rise, recovery periods lengthen, and serious illnesses affect people at younger ages, critical illness insurance has emerged as a vital pillar of long-term financial resilience.

India’s Insurance Reforms: 100% FDI and What It Means

India’s Insurance Amendment Bill: 100% FDI, Strategic Restraint, and a Defining Moment for the Sector

The Indian Union Cabinet’s approval of the Insurance Amendment Bill, raising the Foreign Direct Investment (FDI) limit in insurance companies to 100%, marks one of the most consequential reforms in India’s insurance landscape in decades. At a time when insurance penetration remains structurally low, this policy shift is expected to unlock long-awaited global capital, expertise, and innovation into the sector.

Yet, the reform is not an unqualified liberalization. The exclusion of composite licenses and the absence of an open architecture framework signal a calibrated approach. It balances capital inflows with regulatory discipline. Together, these choices are likely to shape both the short-term competitive dynamics and the long-term evolution of India’s insurance market.

This blog explores what the Insurance Amendment Bill means for investors, insurers, intermediaries, and consumers, and how it could redefine the future of insurance in India.

Key Insight: Capital Infusion Meets Strategic Restraint

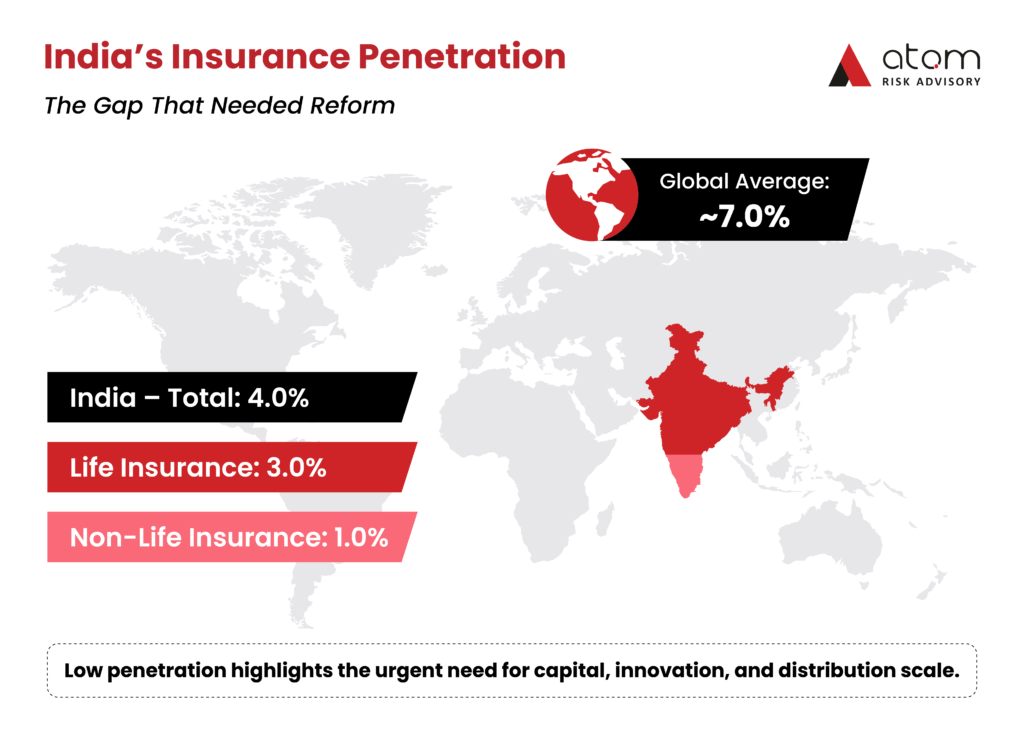

India’s insurance sector plays a vital role in economic resilience and individual financial security, yet it continues to lag global peers on penetration metrics. As of FY 2022-23, India’s overall insurance penetration stood at 4.0%, comprising 3.0% for life insurance and 1.0% for non-life insurance – significantly below the global average of approximately 7.0%.

This persistent gap highlights the urgent need for capital, innovation, and distribution depth. The decision to raise the FDI limit from 74% to 100% directly addresses these constraints.

By allowing full foreign ownership, the amendment is expected to:

- Unlock substantial foreign capital inflows

- Enable existing insurers to strengthen balance sheets and solvency

- Encourage new global insurers to enter the Indian market

- Introduce advanced underwriting practices, risk models, and technology

- Expand the range of products tailored to Indian consumers

However, the Bill’s structural guardrails are just as significant as its liberalization measures.

It excludes the option for composite licenses, meaning insurers cannot offer both life and non-life insurance products under a single entity. This approach promotes specialization, which could help prevent risk concentration and maintain regulatory clarity across distinct product categories.

Additionally, the lack of an open architecture mandate, which would have permitted agents to sell products from multiple insurers freely, suggests a preference for the existing tied-agency model. While this may limit immediate consumer choices and disrupt markets for brokers, it could also foster deeper relationships between insurers and their distribution channels, ensuring focused training and accountability.

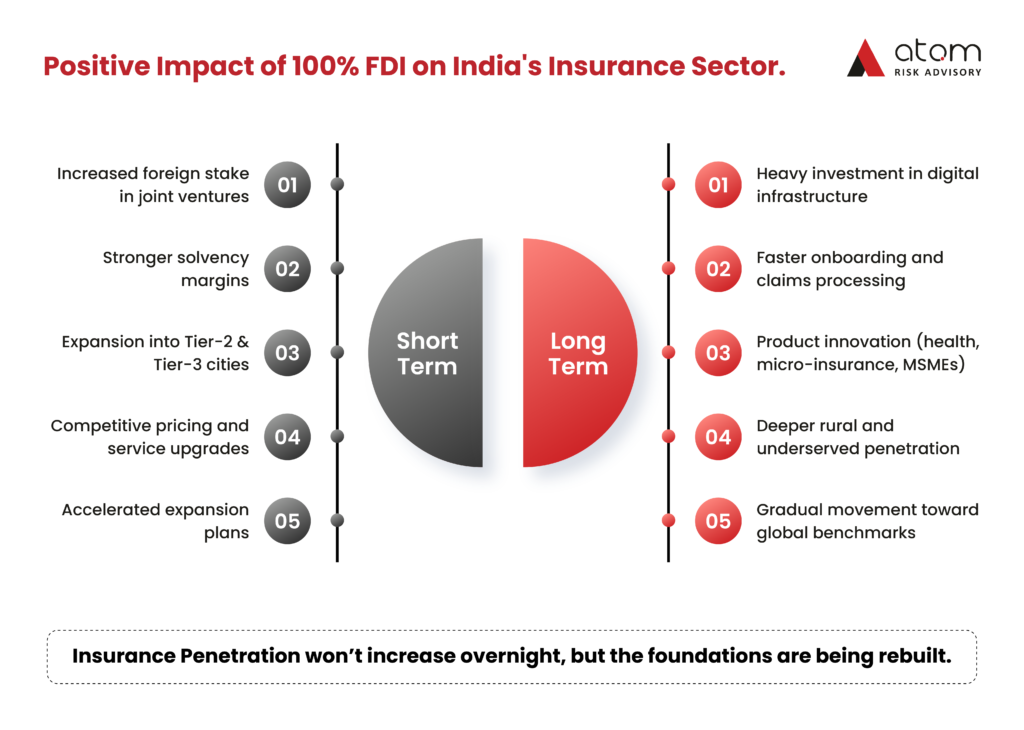

Short-Term Impact: Capital, Competition, and Market Expansion

In the immediate aftermath of the reform, the industry is expected to witness a surge in activity:

- Foreign partners in existing joint ventures may increase their stakes

- Fresh capital infusions are likely to improve solvency margins

- Insurers will expand aggressively into Tier-2 and Tier-3 cities

- Heightened competition may lead to better pricing and improved service standards

- Distribution strategies will remain segmented and specialized across life and non-life businesses

For consumers, this phase is likely to translate into greater accessibility, stronger insurers, and more competitive offerings.

Long-Term Impact: Innovation, Inclusion, and Structural Transformation

Over the long term, the implications of 100% FDI are potentially transformative.

Sustained capital inflows will enable insurers to invest deeply in digital infrastructure, streamlining customer onboarding, underwriting, and claims processing. Technology-led efficiencies are expected to drive:

- Personalized and data-driven policy design

- Faster claims settlement and improved customer experience

- Scalable distribution models for underserved regions

Product innovation is also set to accelerate, with increased focus on:

- Micro-insurance solutions

- Health and wellness-linked products

- Tailored risk solutions for MSMEs

- Insurance offerings designed for rural and semi-urban populations

While insurance penetration may not rise overnight, consistent investment, innovation, and awareness campaigns are expected to gradually move India closer to global benchmarks, strengthening household financial security and economic resilience.

A Measured Reform with Long-Lasting Impact

The Insurance Amendment Bill represents a bold yet balanced step in liberalizing India’s insurance market. By combining full foreign ownership with structural prudence, the government has laid the foundation for sustainable growth rather than short-term disruption.

This reform is not merely about capital infusion. It is about reshaping the insurance ecosystem, fostering innovation, strengthening institutions, and expanding protection across India’s vast and diverse population.

How Atom Risk Advisory Can Help

As India’s insurance landscape evolves, navigating regulatory shifts, capital strategies, and market entry decisions requires deep sector expertise and global perspective.

Atom Risk Advisory works closely with insurers, reinsurers, investors, and intermediaries to help them:

- Assess regulatory and structural implications of reforms

- Design market entry and expansion strategies

- Build compliant, future-ready insurance and risk solutions

- Align global capabilities with India’s unique market dynamics

Connect with Atom Risk Advisory to explore strategic insurance and risk solutions tailored to your long-term objectives.

Movember’s Most Important Lesson

Movember May Be Ending. But Your Health Awareness Journey Shouldn’t.

Movember, famously named by blending “moustache” and “November”, began as a global movement encouraging men to grow a ‘mo’ throughout the month to spark conversations around men’s health. What started as a simple visual cue – a moustache – has grown into one of the world’s most recognizable campaigns spotlighting prostate cancer, testicular cancer, mental health, and suicide prevention. Across November, these moustaches become symbols of awareness, early detection, and open dialogue – reminding men everywhere to prioritize their well-being.

Movember is now drawing to a close. While the moustaches may soon come off, the message behind them should stay with us all year. Awareness is powerful – but taking action is what truly protects you.

Too often, men focus on screenings, symptoms, and mental well-being during Movember, but overlook a critical aspect of long-term health resilience: the financial and lifestyle impact of a serious illness, and the role protection plays in safeguarding your future. As the month wraps up, this is the moment to extend the conversation beyond physical health and into something just as crucial — how a critical illness can reshape your income, lifestyle, and family’s security.

Your ‘mo’ this November wasn’t just a symbol. It was a reminder to look deeper. While we celebrate the awareness Movember spreads, it’s essential to carry forward the message by preparing for realities many men ignore until they’re forced to face them.

Critical Illness: The Men’s Health Wake-Up Call You Can’t Ignore

Imagine this: life is on track, your career is growing, family responsibilities are increasing, and your financial goals are finally taking shape. Then, suddenly, a diagnosis changes everything: cancer, a heart attack, a stroke, or another major illness.

The challenge isn’t only medical. It’s immediately financial.

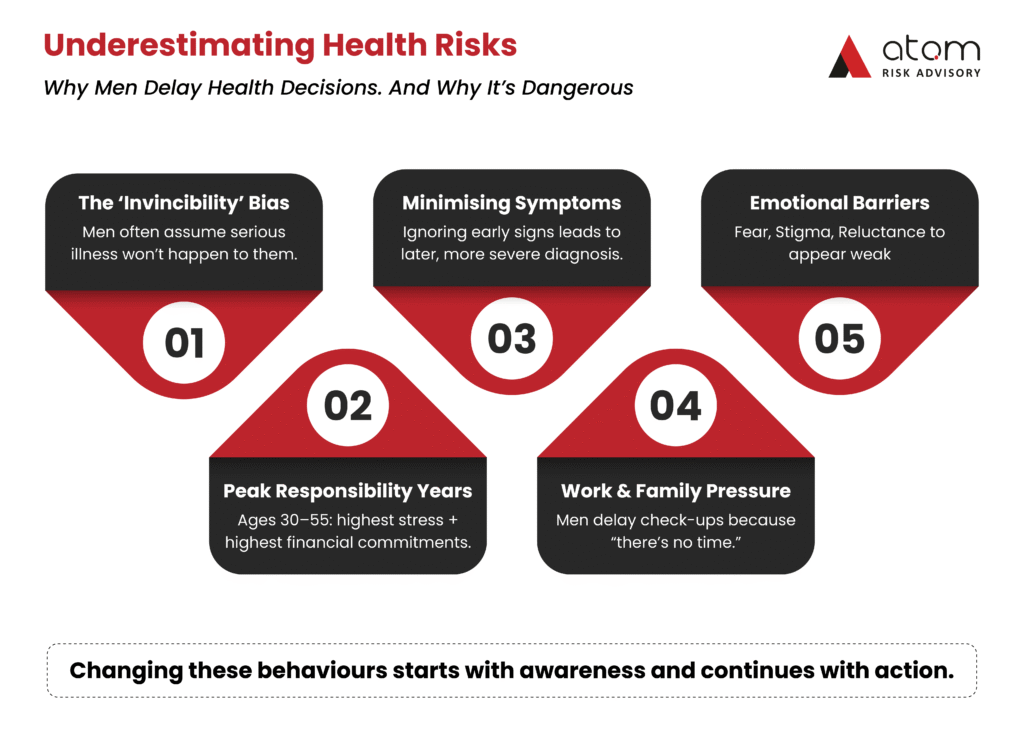

Many men carry a sense of invincibility, believing that serious illness is something that happens later in life, or to someone else entirely. But the reality is very different, and Movember has once again highlighted how essential it is to face the facts.

Here’s what industry data continues to tell us:

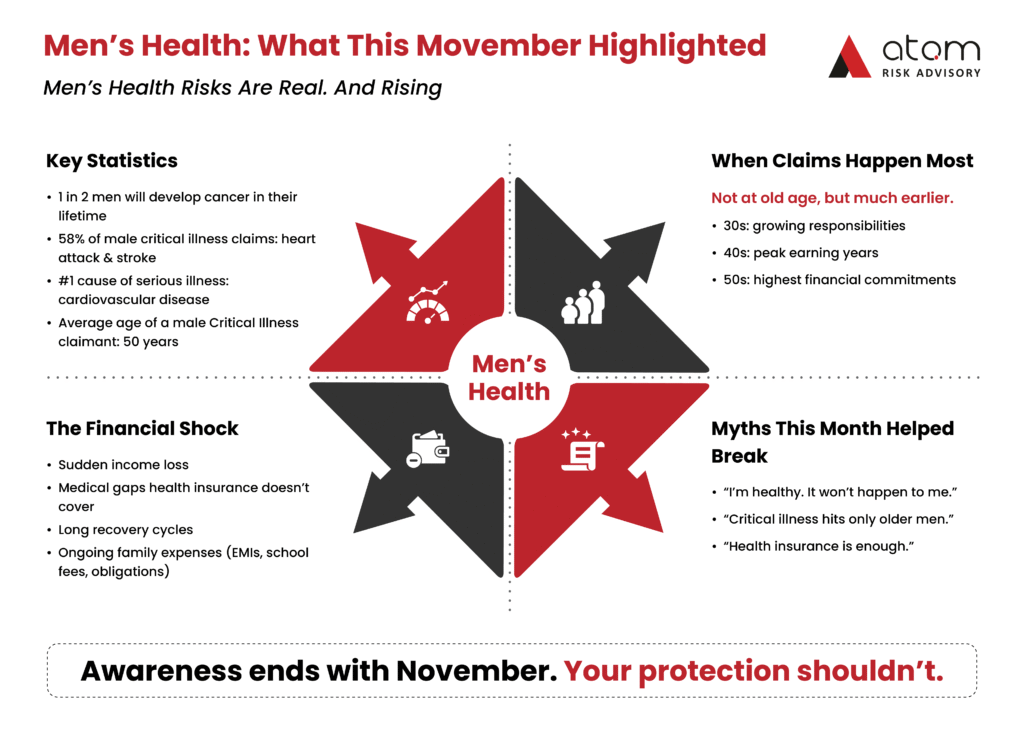

Cancer:

One in two men will be diagnosed with some form of cancer in their lifetime. Survival rates are improving, but the costs – medical, emotional, and financial – remain overwhelming.

Heart Attack & Stroke:

These remain the leading causes of critical illness among men globally. Beyond the physical hardship, they frequently disrupt earning capacity for long periods.

Age of Claims:

Critical illness claims are not dominated by senior citizens.

Insurers globally report a major portion of claims coming from men in their 30s, 40s, and 50s — precisely when mortgages are highest, children are in school, and financial commitments peak.

The Middle East 2025 Customer Claims Paid Report (tracking claims between 2022 and 2024) recorded the average age of a male critical illness claimant at just 50 years. Even more striking: 58% of all critical illness claims for men were due to heart attack and stroke.

These statistics aren’t meant to intimidate; they’re meant to inform. They emphasize that critical illnesses are not distant risks but real, current vulnerabilities that require proactive preparation.

While the physical toll is undeniable, the financial consequences – lost income, mounting bills, home adjustments, recovery costs – can be equally devastating and can derail everything you’ve worked hard to build.

Your Critical Illness Lifeline: Why Protection Matters Even More After Movember

Movember may be ending, but the call to safeguard your future shouldn’t. A moustache lasts 30 days. But the decisions you make today can protect you for decades.

Critical Illness Insurance is more than a policy. It is a strategic, forward-looking safeguard designed to strengthen your financial resilience in the face of severe health challenges.

What exactly is Critical Illness Insurance?

It provides a tax-free lump sum payout upon diagnosis of a covered major illness (such as cancer, heart attack, stroke, multiple sclerosis, and many others). The payout is made immediately on diagnosis, not upon death – giving you the freedom to make decisions based on your health needs, not financial constraints.

Why It Is Essential for Your Future

- Replaces Lost Income

If a critical illness prevents you from working, your income may stop. A lump sum payout ensures your financial responsibilities don’t.

- Covers Unexpected Costs

Health insurance rarely covers everything. Critical Illness Insurance supports private care, specialized treatment, experimental therapies, or travel for global medical options.

- Supports Lifestyle Adjustments

Serious illness may require home modifications or long-term care. CI payouts ensure you can adapt your lifestyle without difficulty.

- Protects Your Family’s Financial Future

From mortgages to children’s education, the payout keeps your family secure during recovery.

- Reduces Stress and Promotes Recovery

Knowing finances are taken care of allows you to focus entirely on healing.

Common Misconceptions. And Why Movember Proved Them Wrong

“I’m healthy. I don’t need it.”

Many claimants were healthy before diagnosis. Protecting yourself while you’re healthy ensures eligibility and lower premiums.

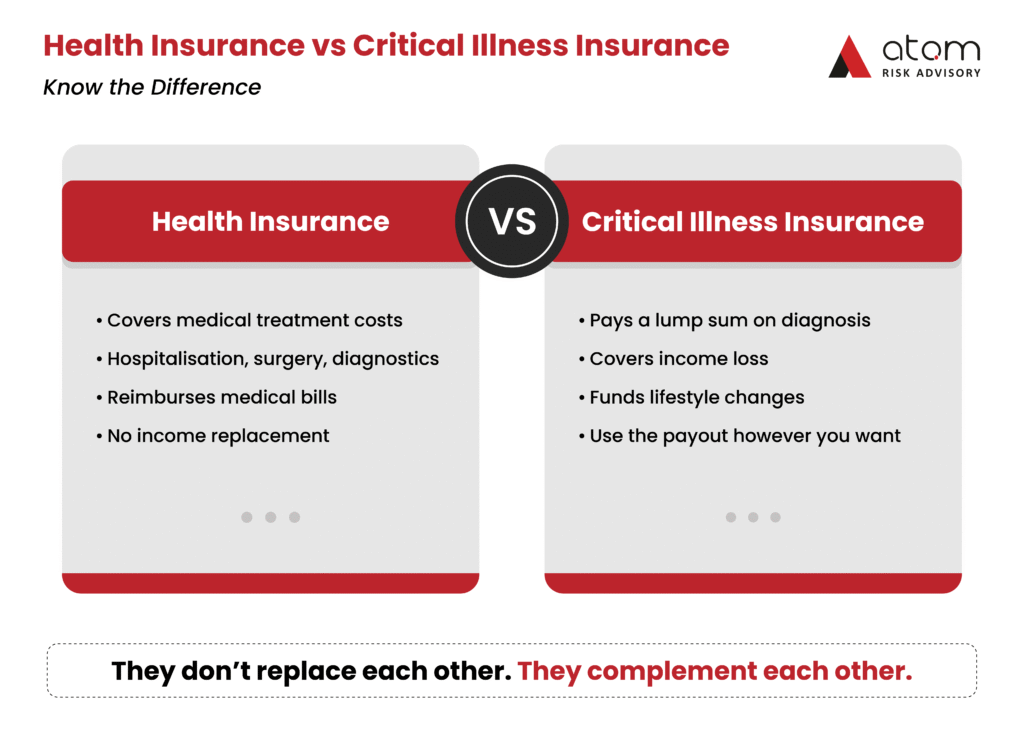

“My health insurance covers everything.”

Health insurance covers medical treatment, not income loss, home changes, or lifestyle support.

The two policies complement each other. They’re not interchangeable.

“It’s too expensive.”

Premiums vary but are often more affordable than assumed, especially compared to the financial fallout of going uninsured.

A Real-Life Perspective

Consider David, 45, a father of two.

A severe cancer diagnosis upended his life. While his health insurance covered treatment, it was his Critical Illness Insurance that truly protected his family – replacing income, supporting childcare, and giving them stability during an incredibly difficult time.

Before November Ends: Take Action That Lasts Beyond Awareness

Movember has reminded us of the importance of conversations around men’s health. But awareness is only powerful when it turns into action; especially action that protects your long-term financial resilience. As the month wraps up, this is the ideal time to review your protection, evaluate your risks, and put a critical illness plan in place.

Your future self, and your family, will thank you.

Take the Next Step Before the Year Ends

At Atom Risk Advisory, our qualified advisors help you understand your coverage needs, compare leading global protection plans, and structure a Critical Illness Insurance strategy that gives you and your family unmatched peace of mind.

Speak to a qualified financial advisor to understand your options, assess your needs, and secure a critical illness insurance plan that offers you and your family the ultimate peace of mind.

Let this Movember be the month you transform awareness into unwavering protection.

PPLI for Global Expats: Protecting Wealth Beyond Borders

Discover how Private Placement Life Insurance (PPLI) helps global expats invest in US markets tax-efficiently, avoid withholding and estate taxes, and protect their wealth across borders. Learn why PPLI is the ultimate strategy for long-term growth and legacy planning.

The #1 Flaw in Most Buy-Sell Agreements – and How to Fix It

Turn your buy-sell agreement from a paper promise into a funded safety net with life and disability insurance to protect partners and families.

Breast Cancer and Financial Protection: Why Women Need Critical Illness Cover

Beyond the Pink Ribbon: Building Your Financial Shield Against Breast Cancer

Breast Cancer. The words alone spark a surge of emotions – fear, uncertainty, resilience.

Every October, the world turns pink to honour survivors, remember those we’ve lost, and advocate for research and early detection.

Yet amid the essential conversations around screenings, treatments, and emotional support, one crucial aspect is often overlooked: the financial impact of a breast cancer diagnosis.

A diagnosis isn’t just a medical journey – it’s a financial one. The cost of care can disrupt families, drain savings, and add immense stress to an already overwhelming experience. At Atom Risk Advisory, we believe true preparedness goes beyond detection; it includes a robust financial shield that allows you to focus on healing.

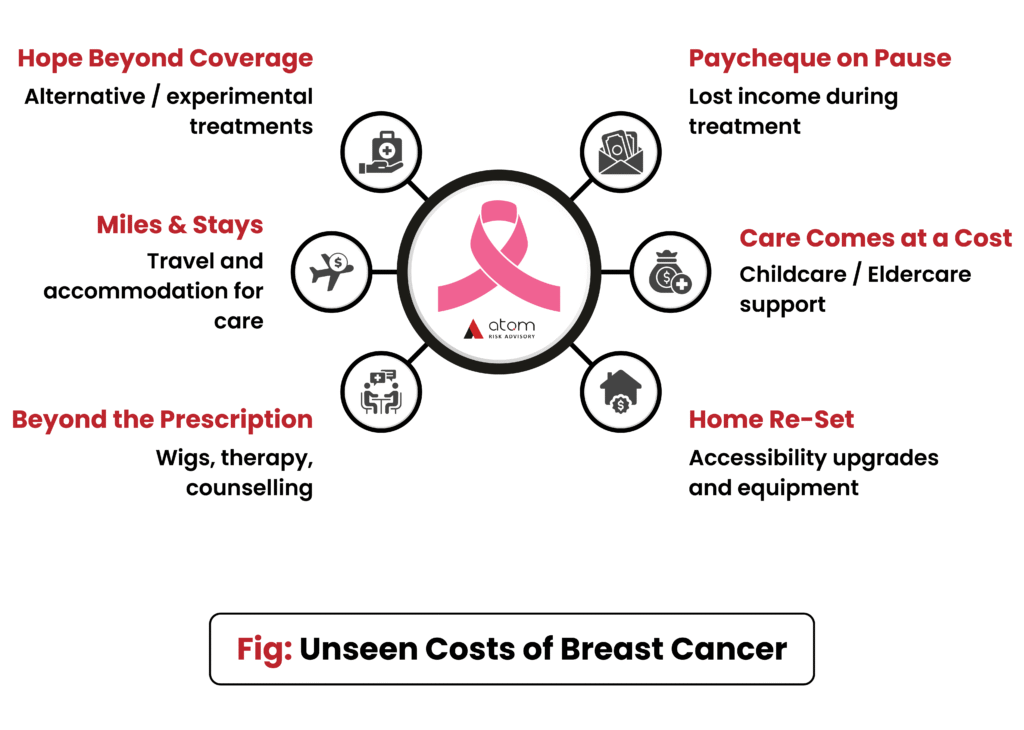

The Unseen Costs of Breast Cancer: More Than Hospital Bills

Even with excellent primary health insurance, the out-of-pocket costs of breast cancer can escalate quickly:

- Lost income: Treatment plans often require weeks or months away from work, which can be devastating for primary earners or single-income households.

- Childcare and eldercare: Balancing caregiving responsibilities during treatment can lead to unexpected expenses.

- Travel and accommodation: Specialist care often requires frequent trips or temporary stays in other cities.

- Specialized needs: Wigs, prosthetics, physical therapy, nutritional plans, mental-health counselling, or home modifications all add up.

- Alternative or experimental treatments: Many advanced or innovative therapies may not be fully covered by traditional health insurance.

This silent financial pressure can weigh heavily on patients and their families – often at a time when their energy should be focused on recovery and well-being.

Why a Financial Shield Is Non-Negotiable

Just as early detection saves lives, early financial planning safeguards stability. Waiting until a diagnosis to plan for these expenses is often too late.

A well-structured financial shield typically includes:

- Comprehensive Health Insurance: Understand your policy’s coverage, deductibles, and exclusions.

- Income Protection / Disability Insurance: Replace part of your income if you’re unable to work during treatment.

- Critical Illness Insurance: Receive a tax-free lump-sum payment upon diagnosis of serious illnesses such as breast cancer, heart attack, or stroke.

- Estate Planning Essentials: Wills, power of attorney, and beneficiary updates bring peace of mind during uncertain times.

The Numbers Speak: Breast Cancer and Women’s Critical-Illness Claims

This Breast Cancer Awareness Month, let’s look beyond the pink ribbon and consider a powerful financial tool: Critical Illness Cover. This type of insurance provides a tax-free, lump-sum payment upon diagnosis of a specified critical illness, such as breast cancer, heart attack, or stroke, as defined in your policy.

What Critical Illness Claims Data Reveals for Women

Claims insight from a leading Insurance provider in the UAE consistently highlights why Critical Illness Cover is so vital, particularly for women. Recent data from the Middle East shows that cancer is the leading cause of critical-illness payouts, accounting for 51% of all claims. Among women, the concentration is even more striking – around 4 out of 5 female claimants, or nearly 80%, received a payout for cancer, with breast cancer being the most common diagnosis. These figures reflect the experiences of thousands of women who relied on this financial support during their most vulnerable time, enabling them to focus on treatment and recovery without the additional burden of financial stress.

This isn’t just a statistic; it represents thousands of women across the country receiving vital financial lifelines during their most vulnerable time. These payouts empower them to make choices that support their health and well-being, without the added stress of financial ruin.

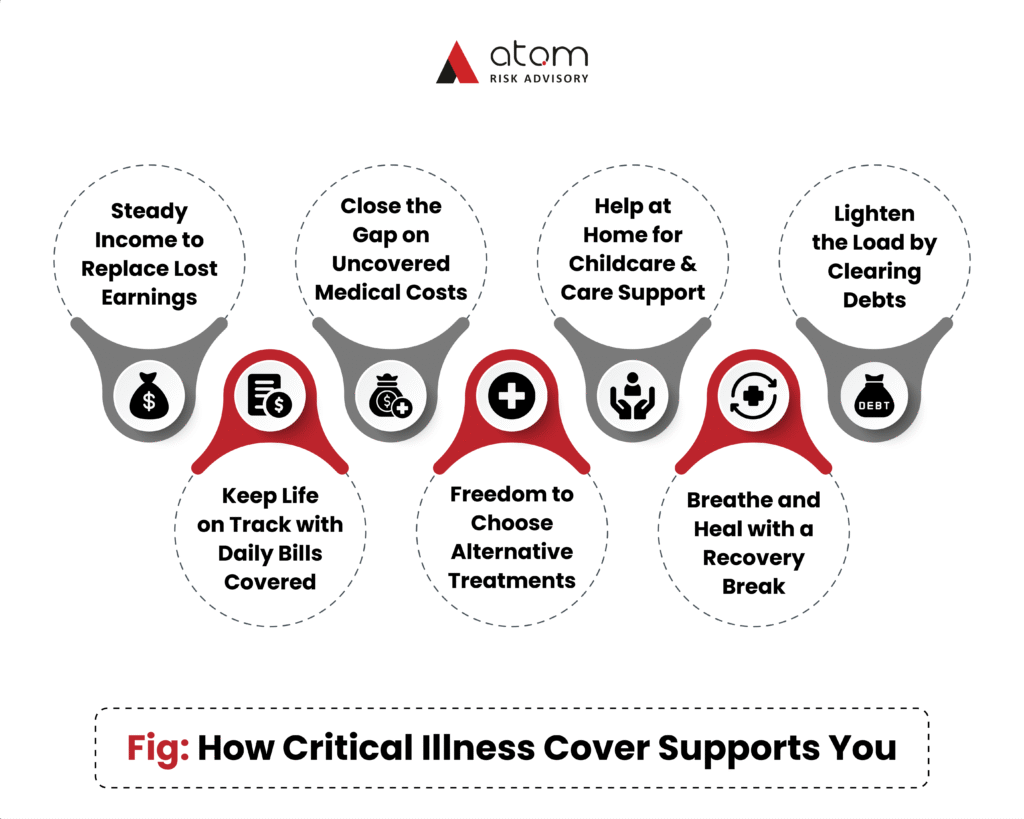

How Critical Illness Cover Works

Unlike standard health insurance, which pays healthcare providers, Critical Illness Cover pays a lump sum directly to you upon diagnosis of a covered condition.

You decide how to use the funds – for medical or non-medical expenses alike:

- Replacing lost income to support your household

- Covering out-of-pocket medical costs not paid by your primary insurance

- Maintaining lifestyle and essential expenses – mortgage, rent, utilities, groceries

- Exploring alternative therapies or clinical trials

- Hiring home care or childcare support

- Reducing debt obligations or even taking a restorative break to boost recovery

This flexibility means you can make health-focused choices without financial compromise.

Taking Action: Building Your Financial Shield

Facing breast cancer is one of life’s toughest challenges – but being financially prepared can bring a sense of control and peace of mind.

Here’s how to get started:

- Review Your Existing Coverage: Understand your health, disability, and critical-illness policies and identify gaps.

- Consult a Financial Advisor: Get professional guidance to create a tailored plan that addresses your needs and risk profile.

- Talk to Your Family: Having open conversations about financial priorities can provide clarity and support during difficult times.

Beyond Awareness: Thriving With Confidence

Breast cancer awareness goes beyond screenings and ribbons – it’s about holistic preparedness.

By proactively building your financial shield, you empower yourself to face the unexpected with confidence, dignity, and focus on healing.

This Breast Cancer Awareness Month, let’s move the conversation from just surviving to truly thriving – protecting not only health but also financial well-being for women and their families.

Ready to Build Your Financial Shield?

At Atom Risk Advisory, we specialize in personalized Critical Illness and Protection solutions designed to safeguard your health, lifestyle, and legacy – wherever you are in the world.

Speak with an Atom Risk Advisory specialist today to review your existing cover, identify gaps, and create a protection plan tailored to you and your family. Your health deserves focus. Your finances deserve protection. Atom Risk Advisory helps you secure both.

Designing Equal Legacies with Life Insurance

Discover how life insurance balances inheritances and protects family unity – an essential tool for estate equalization and long-term succession planning

PPLI: Unlocking the Full Potential of Wealth and Legacy

Demystifying PPLI

A Strategic Tool for Enhanced Wealth Growth and Protection

In today’s complex and ever-evolving world of wealth management, identifying strategies that not only preserve but also significantly enhance your legacy can feel like a continuous challenge. Many sophisticated tools exist, yet some of the most powerful often remain shrouded in complexity, known only to a select few.

One such invaluable, yet often misunderstood, instrument is Private Placement Life Insurance (PPLI). This exclusive tool is a key to unlocking a new realm of possibilities for high-net-worth individuals and families seeking advanced solutions for growth, protection, and intergenerational wealth transfer.

At Atom Risk Advisory, we are experts in cutting through the jargon to highlight how PPLI can reshape the future of your wealth.

In this blog, we’re diving into PPLI, exploring how this unique structure works and why it might be the strategic solution your portfolio needs.

What is Private Placement Life Insurance (PPLI)?

In essence, PPLI is a highly customised, institutionally priced life insurance policy designed specifically for high-net-worth (HNI) and ultra-high-net-worth (UHNI) individuals and family offices. Unlike the retail life insurance products available to the general public, PPLI is a “private placement”, which means it’s not publicly offered and is tailored to the specific needs and investment objectives of a qualified investor.

Think of PPLI not as a mere insurance policy, but as a sophisticated financial wrapper around a bespoke investment portfolio. While it includes a death benefit, its primary appeal for many lies in its ability to facilitate tax-efficient growth and asset protection across a broad spectrum of investments.

How PPLI Works: The Mechanics Behind the Power

A PPLI policy consists of two main components:

- The Insurance Contract: This is the legal agreement with an insurance carrier, providing a death benefit and a cash value component. The cash value is where the investment magic happens.

- The Investment Portfolio: This is where the true flexibility emerges. Unlike traditional variable universal life policies that offer a limited menu of publicly traded mutual funds and/or indexed funds, PPLI allows access to a much broader array of investment options. These can include hedge funds, private equity, real estate funds, and other alternative investments managed by institutional-grade managers, often with lower fees than their retail counterparts. The policyholder typically works with an investment advisor to select and manage these underlying investments, though the actual “owner” of the investments for tax purposes is the insurance carrier.

The crucial element is that the investment gains within the policy’s cash value grow on a tax-deferred basis. When structured correctly, policyholders can access these funds during their lifetime through tax-free withdrawals and loans, and upon death, the proceeds are typically paid to beneficiaries free of income and estate taxes.

The Strategic Advantages: Growth, Protection, and Legacy

PPLI’s value lies in its multi-dimensional benefits, making it one of the most versatile tools in advanced wealth planning:

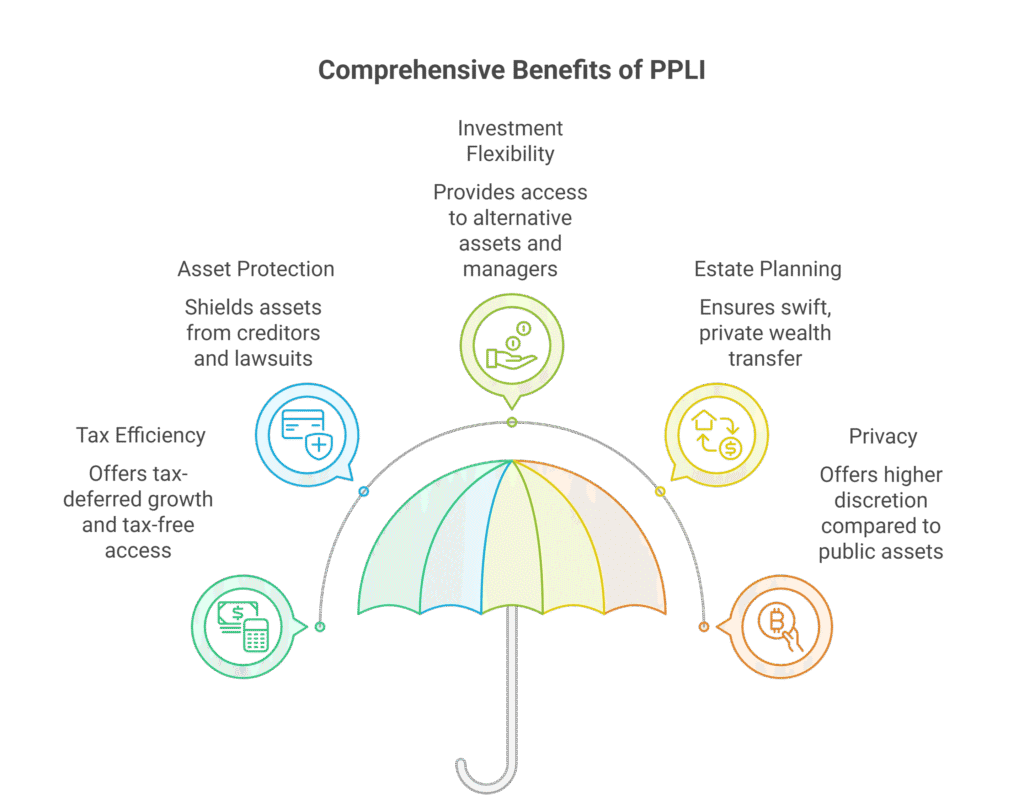

Unparalleled Tax Efficiency:

- Tax-Deferred Growth: Investments within the policy accumulate earnings without annual taxation, allowing for compounding growth over time.

- Tax-Free Access (Potentially): Policyholders can often access the cash value through withdrawals up to their basis and through policy loans, both of which can be tax-free if structured properly.

- Tax-Free Death Benefit: Proceeds generally pass to beneficiaries, income-tax-free, offering liquidity for estate taxes or other obligations.

Robust Asset Protection: Depending on jurisdiction, the cash value within a PPLI policy can be shielded from creditors, lawsuits, or bankruptcy claims – adding an extra layer of security.

Investment Flexibility and Access: Access to a wider universe of alternative assets and top-tier managers allows for bespoke portfolio construction beyond the constraints of public markets.

Streamlined Estate Planning: PPLI bypasses probate, ensuring a swift, private transfer of wealth across generations. Its tax-free death benefit also provides liquidity to cover estate obligations while preserving illiquid assets.

Enhanced Privacy: For families that value confidentiality, PPLI structures offer a higher level of discretion compared to publicly disclosed assets.

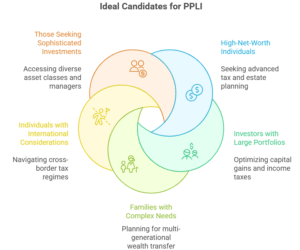

Who is PPLI For?

PPLI is not a one-size-fits-all solution. It’s best suited for:

- High and Ultra-High-Net-Worth Individuals: Those with substantial liquid assets seeking advanced tax and estate planning strategies.

- Investors with Large, Appreciated Portfolios: Individuals seeking to optimize their management of capital gains and income taxes.

- Families with Complex Estate Planning Needs: Those aiming for multi-generational wealth transfer, charitable giving, or providing for dependents with special needs.

- Individuals with International Considerations: PPLI can be particularly effective for cross-border planning, navigating different tax regimes, and maintaining compliance.

- Those Seeking Sophisticated Investment Opportunities: Investors looking for access to a broader range of asset classes and institutional managers.

Important Considerations

While PPLI offers transformative advantages, it also demands careful consideration:

- Significant initial premium commitments.

- Ongoing policy and management fees.

- A long-term horizon – benefits maximize over extended periods, making it a solid investment in the long run .

- Strict adherence to regulatory rules, including investor control guidelines.

For these reasons, navigating the intricacies and successful implementation requires collaboration with specialized advisors and experienced structuring teams.

Its effectiveness hinges on careful structuring, adherence to guidelines (particularly the “investor control” rules), and ongoing management by experienced professionals.

Is PPLI the Strategic Solution Your Portfolio Needs?

PPLI represents a sophisticated approach to wealth management, offering a unique blend of tax efficiency, asset protection, and investment flexibility that few other tools can match. It is a strategic architecture for wealth and testament to strategic foresight and meticulous planning.

If you’re seeking to enhance your wealth structure with growth, resilience, and legacy preservation and seamless wealth transfer, PPLI may be the missing piece.

At Atom Risk Advisory, our role is to demystify complex financial instruments and tailor them to align with your family’s aspirations.

Ready to Unlock the Potential?

We invite you to schedule a confidential consultation with one of our seasoned wealth advisors and our in-house Chief Investment Officer. Together, we can help you cut through complexity and unlock the full power of your wealth.