Bullet-Proof Your Buy-Sell Agreement: Fix the #1 Flaw Most Businesses Overlook

Your business is more than just a venture; it’s a living entity – an engine of growth, a source of livelihood, and often, a cherished legacy. As a business owner, you pour your heart and soul into building it, protecting its present, and planning for its future.

A buy-sell agreement is one of the most critical yet overlooked tools in that planning process. This legally binding contract ensures smooth transitions in ownership when an owner retires, becomes disabled, or passes away unexpectedly.

While most savvy business owners recognize the importance of having a buy-sell agreement in place, many fail to address its biggest vulnerability: funding the buyout when the time comes. Without a clear funding mechanism, even the most carefully drafted agreements can unravel when put to the test. To truly “bulletproof” your buy-sell agreement and eliminate the most significant point of failure, you have to address one key gap that’s often ignored: the source of funds to carry out the buyout.

The Achilles’ Heel of Many Buy-Sell Agreements

Picture this scenario: you and your partners have a meticulously drafted buy-sell agreement that accounts for every detail – from valuation methods to timelines for a buyout. Then the unthinkable happens: a partner passes away or becomes permanently disabled.

Suddenly, the agreement faces its ultimate test. The surviving owners are contractually obligated to purchase the departing owner’s share from their family, or the business itself must redeem those shares. The pressing question arises:

- Do the surviving partners have hundreds of thousands, or even millions, of dollars in liquid assets available on short notice?

- Can the business take on significant debt without jeopardizing its creditworthiness or operations?

- Will the deceased owner’s family be forced to wait for payments, facing potential financial hardship or legal disputes?

- Could the absence of immediate funding force a rushed sale of the entire business, undermining years of hard work and affecting employees’ livelihoods?

This gap in funding is a critical vulnerability that can derail even the strongest agreements. Without a guaranteed source of capital, businesses risk legal battles, operational disruption, and in worst-case scenarios, the loss of the business itself.

Safeguarding Your Business Legacy with Smart Funding Strategies

Life Insurance: The Essential Safeguard

The most effective way to “bullet-proof” your buy-sell agreement is to secure life insurance, and equally important, disability insurance, as an integral funding mechanism.

Here’s why life insurance is a vital component for buy-sell funding:

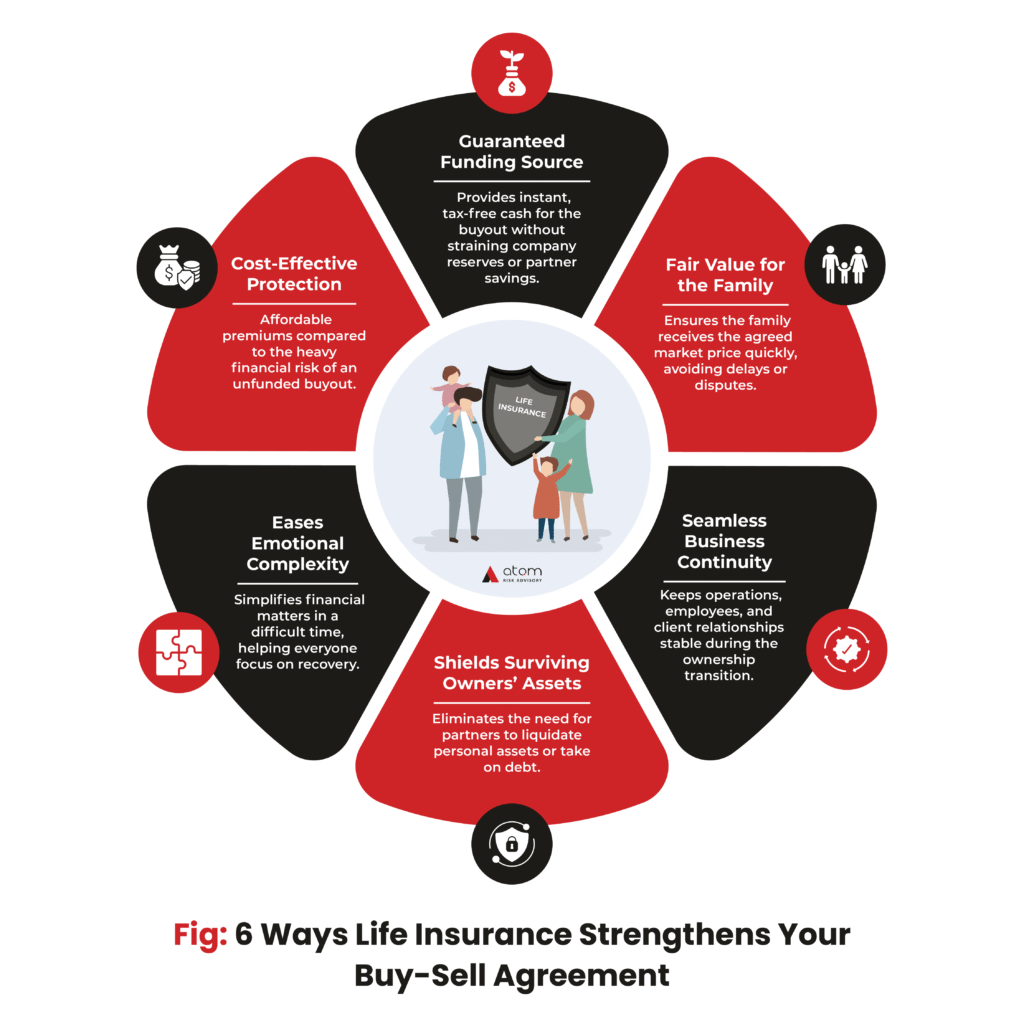

- Guaranteed Funding Source:

When an owner passes away, a life insurance policy on that owner provides immediate, tax-free funds to execute the buyout. This ensures surviving owners can fulfill their contractual obligations without tapping into company reserves, taking on debt, or using personal savings. - Ensures Fair Value for the Family:

The deceased owner’s family receives the agreed-upon market value for their share—at a time when they’re often financially and emotionally vulnerable. This avoids forced sales or undervaluation disputes. - Maintains Business Continuity:

With funding secured, the business transitions ownership smoothly without disrupting day-to-day operations, employee morale, or client confidence. - Protects Personal Assets of Surviving Owners:

Without life insurance, surviving owners might have to liquidate personal assets or incur personal debt to honour the agreement. Insurance shields them from this financial burden. - Simplifies a Complex, Emotional Process:

Grief is challenging enough; adding financial uncertainty intensifies the stress. Life insurance simplifies the process, allowing everyone to focus on healing and stability. - Cost-Effective Risk Management:

Compared to the potential cost of an unfunded buyout, life insurance premiums are a remarkably affordable solution to mitigate a high-stakes risk.

Structuring the Right Policy: Cross-Purchase vs. Entity-Purchase

Life insurance can be tailored to fit the two most common buy-sell structures:

- Cross-Purchase Agreement:

Each owner buys a life insurance policy on every other owner. If one passes away, the surviving owners receive the policy proceeds and use them to purchase the deceased owner’s shares from the estate. - Entity-Purchase (or Redemption) Agreement:

The business itself takes out a life insurance policy on each owner. If an owner passes away, the business receives the policy proceeds and redeems the deceased owner’s shares from the estate.

Don’t Overlook Disability Protection

While death is permanent, a permanent disability can be equally disruptive. A disabled owner might still draw a salary or expect profit distributions without contributing to the business’s growth.

Integrating disability buy-sell insurance ensures there’s funding available for a fair buyout in these “living death” situations – protecting both the business and the disabled owner.

Take Action: Secure Your Business’s Future

Your buy-sell agreement reflects your foresight and commitment to your business’s longevity. But without adequate funding, it remains just an aspiration.

Here’s how you can safeguard your business’s future today:

- Review Your Existing Buy-Sell Agreement:

Does it explicitly address how a buyout will be funded? - Assess Your Current Needs:

Calculate the coverage required to buy out an owner at fair market value. - Consult with Experts:

Collaborate with your financial advisor, insurance specialist, and legal counsel to design a life and disability insurance plan that integrates seamlessly with your agreement—protecting your business, your partners, and your families.